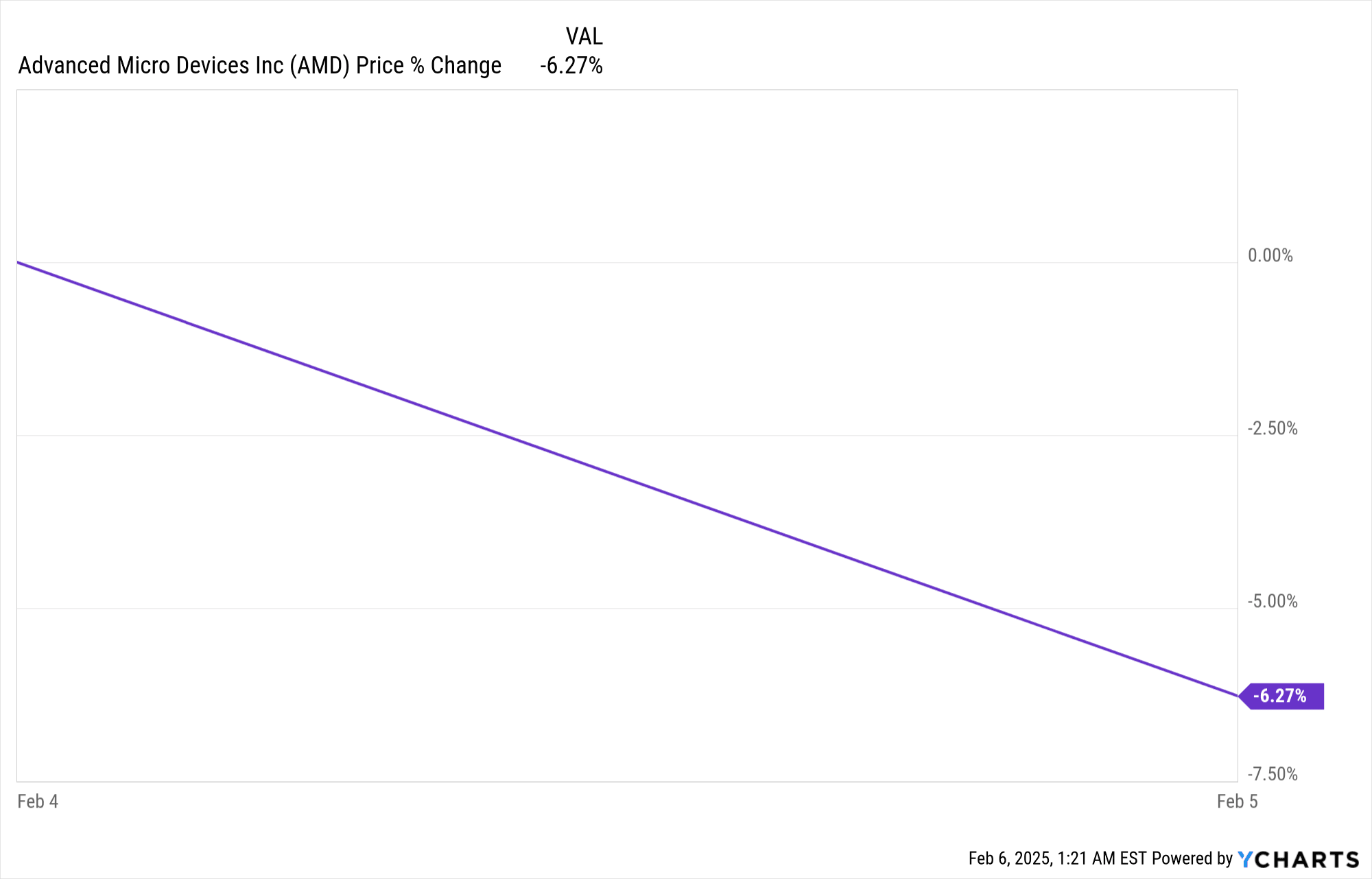

AMD stock rose 6.3% post-earnings, reflecting mixed financial results. Q4 2024 revenue hit $7.66B, exceeding estimates by $132M with 24% YoY growth. Normalized EPS matched forecasts at $1.09, but GAAP EPS of $0.29 missed by $0.31. Data Center revenue soared 69% YoY to $3.9B, offsetting a 59% gaming decline. Gross margin expanded 330 bps YoY to 54%, driven by higher-margin AI and cloud sales.

Source: Ycharts.com

I. AMD Earnings Overview Q4 2024

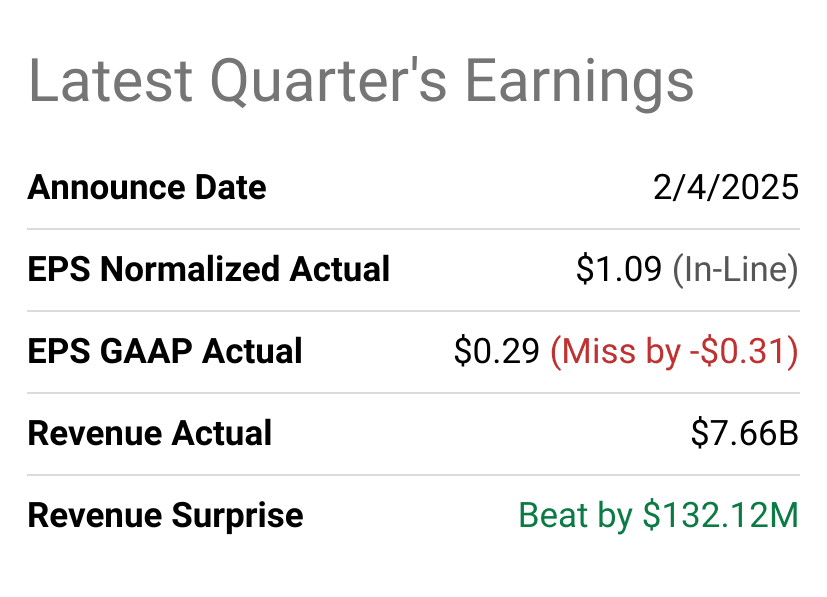

Earnings Vs. Expectations

AMD’s Q4 2024 earnings, announced on February 4, 2025, showcased a mixed performance. Revenue reached $7.66 billion, surpassing expectations by $132.12 million, marking a 24% year-over-year (YoY) growth. However, normalized EPS of $1.09 was in line with expectations, while GAAP EPS of $0.29 missed by $0.31. Net income growth was driven by strong performance in the Data Center and Client segments, which offset declines in Gaming and Embedded segments. Gross margins expanded by 330 basis points YoY to 54%, reflecting a favorable revenue mix shift toward higher-margin data center and client products.

Source: seekingalpha.com

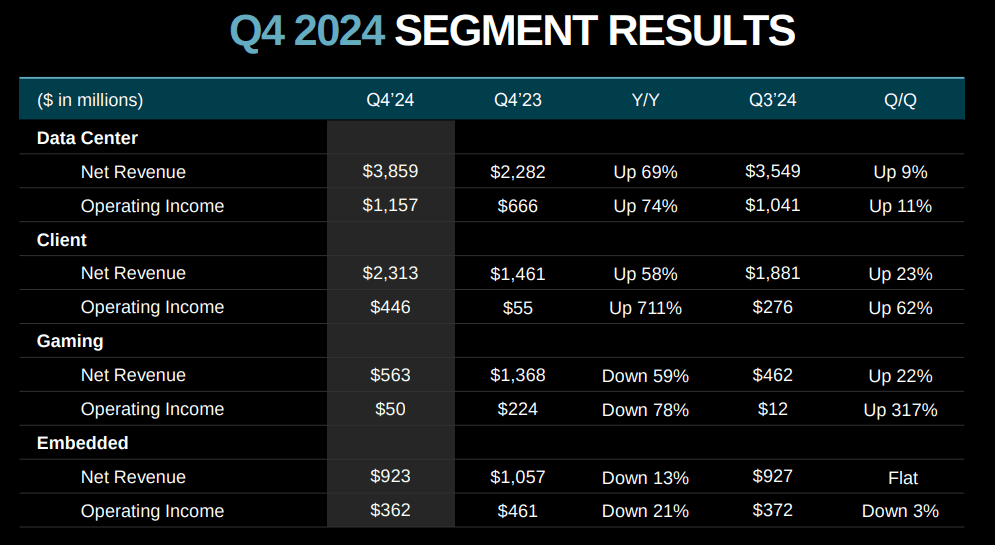

AMD Earnings Q4 2024 Revenue Breakdown and Market Performance

AMD’s record Q4 revenue was primarily driven by its Data Center and Client segments. Data Center revenue grew 69% YoY to $3.9 billion, fueled by strong demand for EPYC CPUs and Instinct GPUs. The segment benefited from hyperscaler adoption, with AMD securing over 50% market share at major hyperscale customers. EPYC CPU sales grew double-digits YoY, driven by the ramp of fifth-gen EPYC Turin processors and expanded cloud deployments. Public cloud instances powered by EPYC increased 27% YoY to over 1,000, with major cloud providers like AWS, Microsoft, and Google launching over 100 AMD-powered instances in Q4 alone.

The Client segment revenue grew 58% YoY to $2.3 billion, driven by strong demand for Ryzen processors. AMD gained market share in both desktop and mobile CPUs, with Ryzen processors dominating retail sales during the holiday season. The segment also saw growth in AI-enabled PCs, with AMD being the sole provider of CPUs enabling Windows Copilot+ experiences. In contrast, the Gaming segment revenue declined 59% YoY to $563 million, due to reduced semi-custom sales as Microsoft and Sony focused on clearing console inventory. The Embedded segment revenue fell 13% YoY to $923 million, impacted by slower recovery in industrial and communications markets.

Source: Q4 Earnings Slides

Data Center AI Momentum

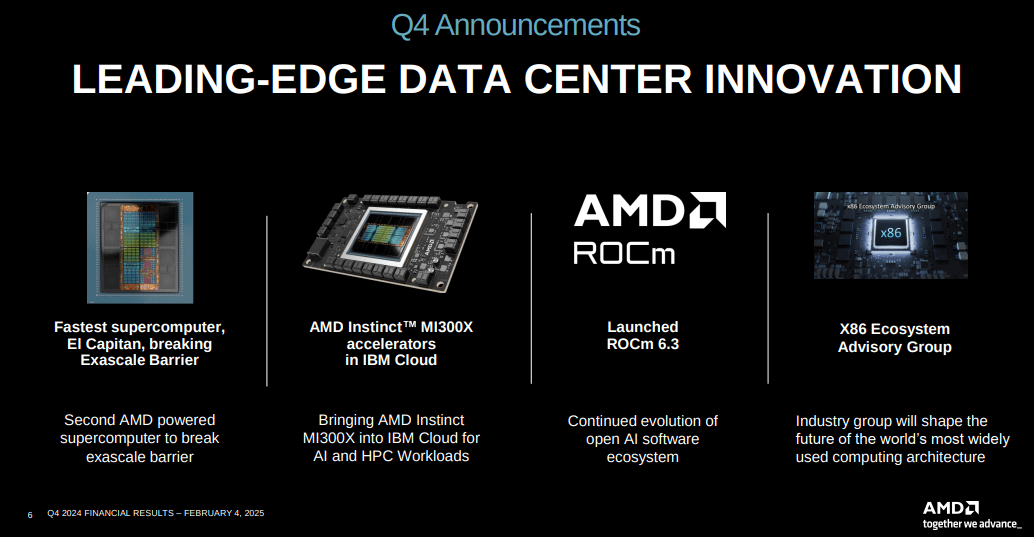

AMD’s Data Center AI business achieved over $5 billion in revenue for 2024, driven by the MI300X accelerator. Key deployments included Meta using MI300X for its Llama 405B model and Microsoft powering GPT-4-based Copilot services. AMD also expanded its ROCm software ecosystem, with ROCm 6.3 delivering a 2.7x improvement in MI300X inferencing performance since launch. Looking ahead, AMD plans to sample its next-gen MI350 series in Q1 2025, with CDNA 4 architecture promising a 35x AI performance leap over CDNA 3.

II. AMD Product & Market Dynamics

New Products & Innovations and Market Reception

AMD’s product strategy in Q4 2024 demonstrated a strong focus on leadership in data center AI, client CPUs, and gaming GPUs. A key highlight was the expansion of its data center AI franchise, which generated over $5 billion in revenue, emphasizing AMD’s aggressive push into AI acceleration. The MI300X accelerators gained traction among major cloud service providers (CSPs) such as Microsoft, Meta, IBM, and Tencent, with Meta using MI300X for its Llama 405B model and Microsoft leveraging it for GPT-4-based Copilot services. AMD’s early silicon validation for MI350 suggests a significant leap in AI performance, expected to increase compute capability 35x compared to CDNA 3.

Source: Q4 Earnings Slides

In the server CPU market, AMD's fifth-generation EPYC “Turin” processors established dominance, surpassing 50% share at the largest hyperscalers. The company's focus on AI-driven cloud computing resulted in a 69% YoY increase in data center revenue, reaching $3.9 billion. The launch of 120 new Turin platforms by major OEMs like Dell, Lenovo, and HPE reinforced its competitive standing. Additionally, the EPYC platform adoption among enterprises tripled, with Visa, Verizon, and Hitachi deploying AMD-based infrastructure at scale.

In the client market, Ryzen desktop and mobile processors drove a 58% YoY revenue surge to $2.3 billion. AMD's dominance in retail channels was evident with over 70% share at Amazon and Newegg, while its strategic partnership with Dell marked a significant expansion into commercial PC markets. The launch of 22 new Ryzen processors, including AI-optimized models, showcased AMD’s commitment to the AI PC segment.

Competitive Landscape

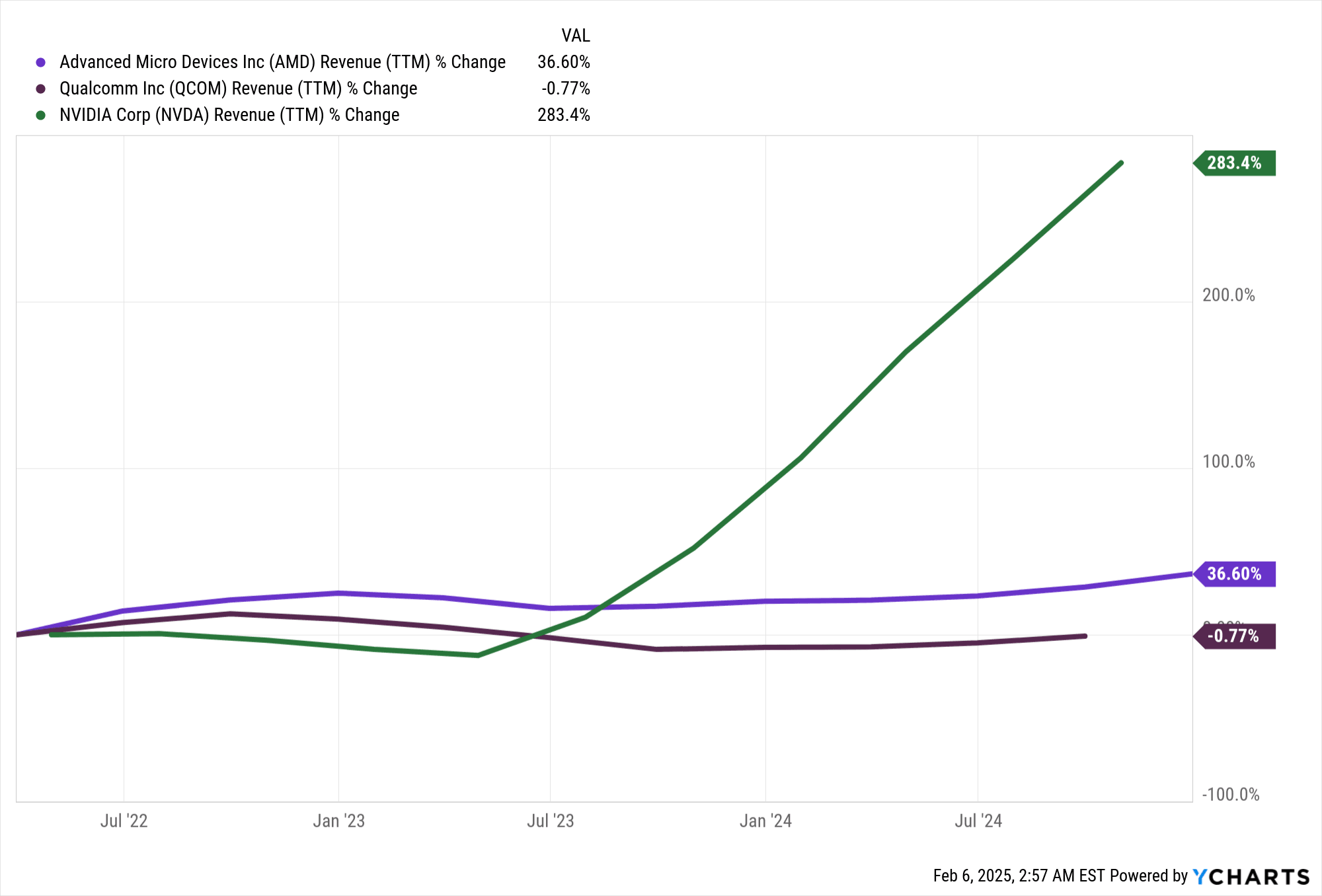

AMD's growth trajectory in Q4 2024 placed it in direct competition with Intel, Nvidia, Qualcomm, and ARM-based chipmakers. The data center segment saw notable market share gains against Intel, as EPYC CPUs continued to outperform Xeon alternatives in performance-per-watt and total cost of ownership. The introduction of HBM-powered EPYC processors with 8x memory bandwidth compared to competitors further solidified AMD’s lead in high-performance computing (HPC) and AI workloads.

Source: Ycharts.com

Nvidia remains the dominant player in AI accelerators, but AMD’s MI300 series, with ROCm optimizations and enterprise-friendly software enhancements, represents a credible alternative. The company’s rapid iteration with MI325 and MI350 further intensifies competition in AI training and inference markets.

In gaming, AMD’s Radeon segment suffered a 59% YoY revenue decline to $563 million due to soft semi-custom sales from Microsoft and Sony. However, AMD’s upcoming Radeon 9000 series, featuring improved ray tracing and AI upscaling, aims to regain ground against Nvidia’s RTX offerings. Meanwhile, the embedded segment declined 13% YoY, indicating market headwinds in industrial and communications sectors.

AMD’s pricing strategy in 2024 balanced premium and mainstream offerings, positioning EPYC CPUs and MI300 accelerators as high-value alternatives to Intel and Nvidia, while Ryzen maintained competitive consumer pricing. Looking forward, AMD’s aggressive R&D investments and sustained product leadership position it for continued market share expansion in 2025.

III. AMD Stock Forecast 2025

AMD Stock Prediction Technical Analysis

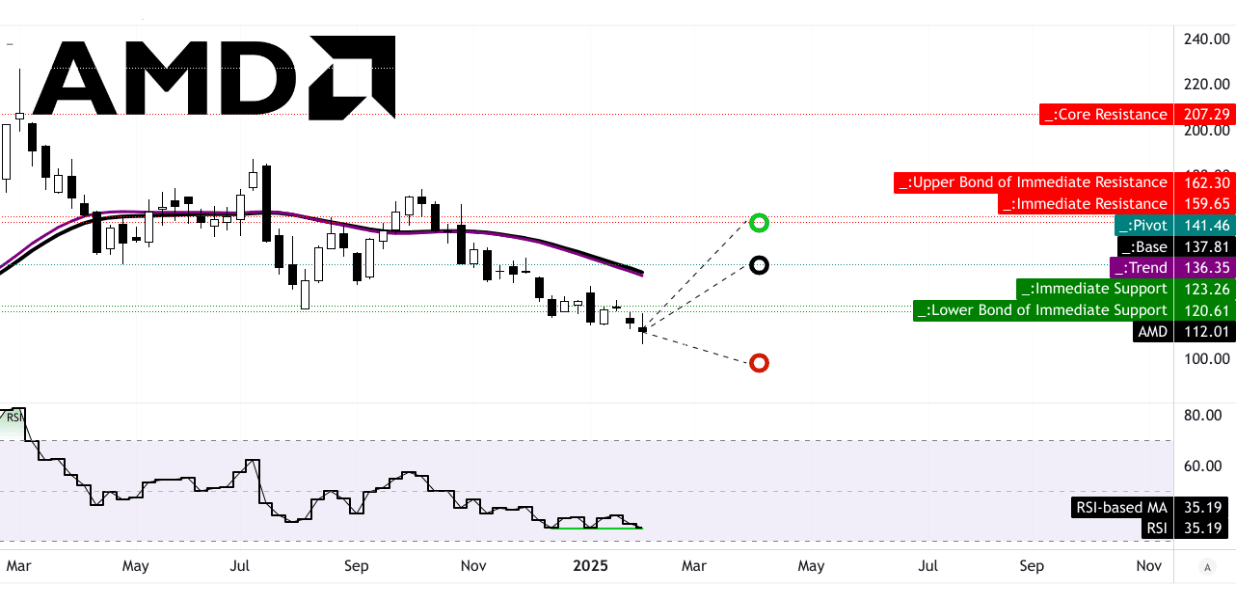

AMD’s stock is currently priced at $112, sitting significantly below both the trendline ($136.35) and baseline ($137.81), as defined by modified exponential moving averages. This suggests a strong bearish deviation from historical moving averages. The average price target for Q1 2025 is projected at $141, supported by a momentum-driven change-in-polarity assessment applied to Fibonacci retracement and extension levels. The optimistic scenario places AMD at $160, assuming the current upward price momentum continues. Conversely, the pessimistic case sees AMD dropping to $98, following downward price momentum trends within the same Fibonacci framework.

AMD’s pivot level for the current horizontal price channel is $141.46, indicating a key resistance point. Should AMD break above this level, further bullish movement could be anticipated. The Relative Strength Index (RSI) stands at 35.19, which signals oversold conditions, potentially foreshadowing a price rebound. Notably, bullish divergence is present, meaning the RSI is showing higher lows despite the stock’s downward price action, reinforcing the possibility of an upcoming reversal. There is no bearish divergence, and the RSI trend remains sideways, indicating consolidation before a potential breakout.

Source: tradingview.com

AMD Stock Forecast: Market Analysts' Expectations & Ratings

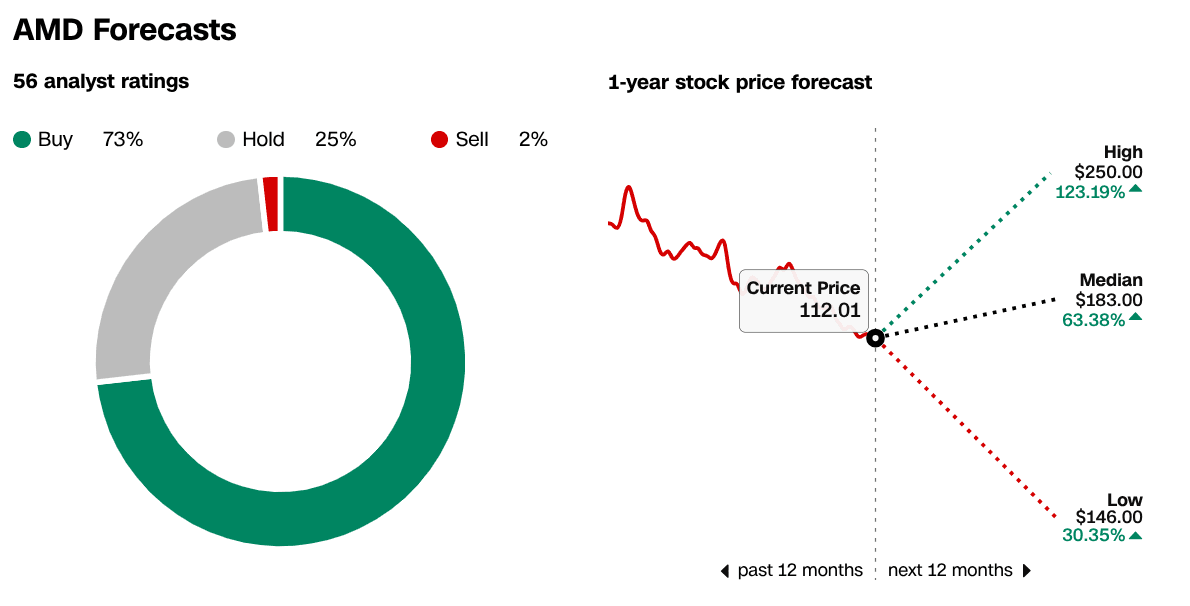

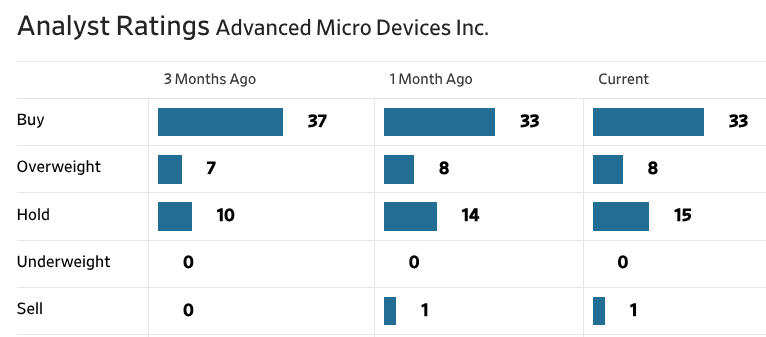

AMD’s stock forecast remains bullish, with 73% of analysts rating it a “Buy,” 25% suggesting “Hold,” and only 2% recommending “Sell.” Over the next 12 months, price targets range from $146 (30.35% upside) to $250 (123.19% upside), with a median estimate of $183 (63.38% upside). The stock currently trades at $112.

Recent rating trends show stability in bullish sentiment. Over the past three months, “Buy” ratings declined from 37 to 33, while “Hold” increased from 10 to 15. The “Overweight” category rose from 7 to 8, and a single “Sell” rating emerged. These shifts indicate cautious optimism, with some analysts tempering expectations.

Price targets reflect strong growth prospects, driven by AI, data center expansion, and competitive positioning against Nvidia and Intel. However, macroeconomic conditions and execution risks could impact these forecasts, making it crucial for investors to monitor earnings reports and industry trends closely.

Source: CNN.com

Source: WSJ.com

IV. AMD Stock Forecast: Future Outlook

Management’s Growth Forecasts and Strategic Initiatives

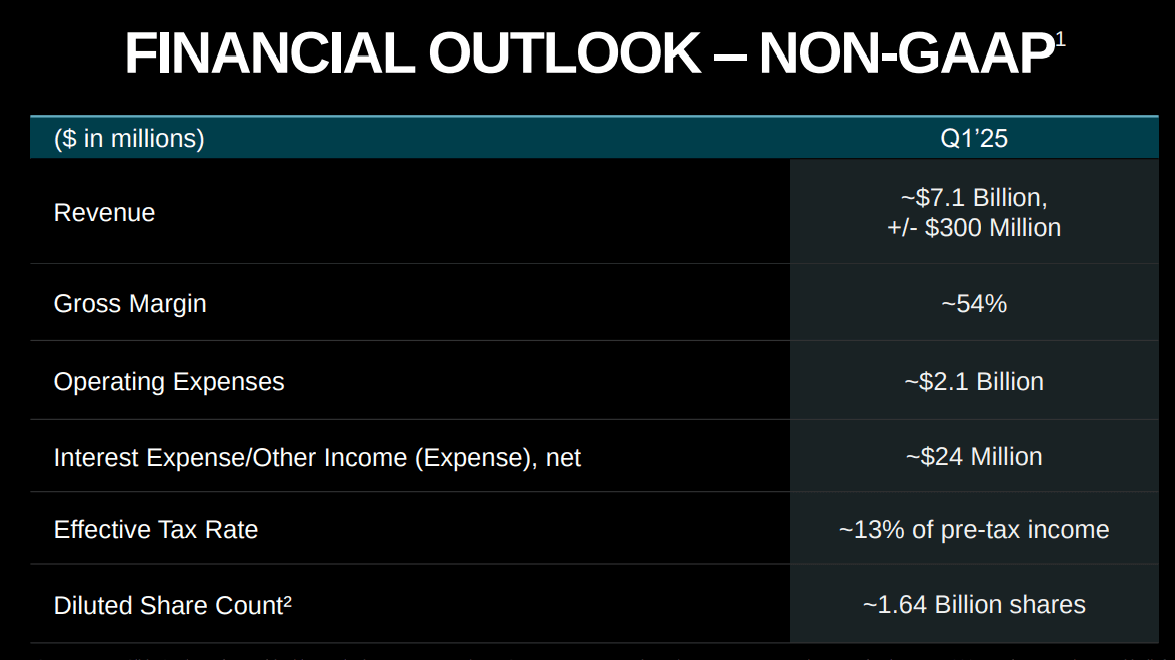

AMD’s Q4 2024 earnings report highlighted the company’s ability to deliver record revenue of $7.7 billion, a 24% YoY increase. More notably, AMD’s data center segment revenue surged 69% YoY to $3.9 billion, underlining the company’s leadership in AI and cloud computing. The company has projected a 29.77% YoY increase in revenue for FQ1 2025, reaching $7.1 billion, alongside an impressive 51.27% YoY increase in EPS to $0.94. This signals confidence in sustained growth, driven by continued AI expansion and server market penetration.

Source: Q4 Earnings Slides

Strategically, AMD is capitalizing on strong demand for EPYC processors in cloud and enterprise sectors, with over 50% share at major hyperscale customers. Additionally, the AI business is thriving, with more than $5 billion in data center AI revenue for 2024. The Instinct MI300X accelerator has gained traction with industry leaders like Meta, Microsoft, and IBM, and the upcoming MI350 series promises a 35x improvement in AI compute performance compared to its predecessor. These initiatives position AMD to capture a significant share of the growing AI infrastructure market.

Market Trends Supporting Growth

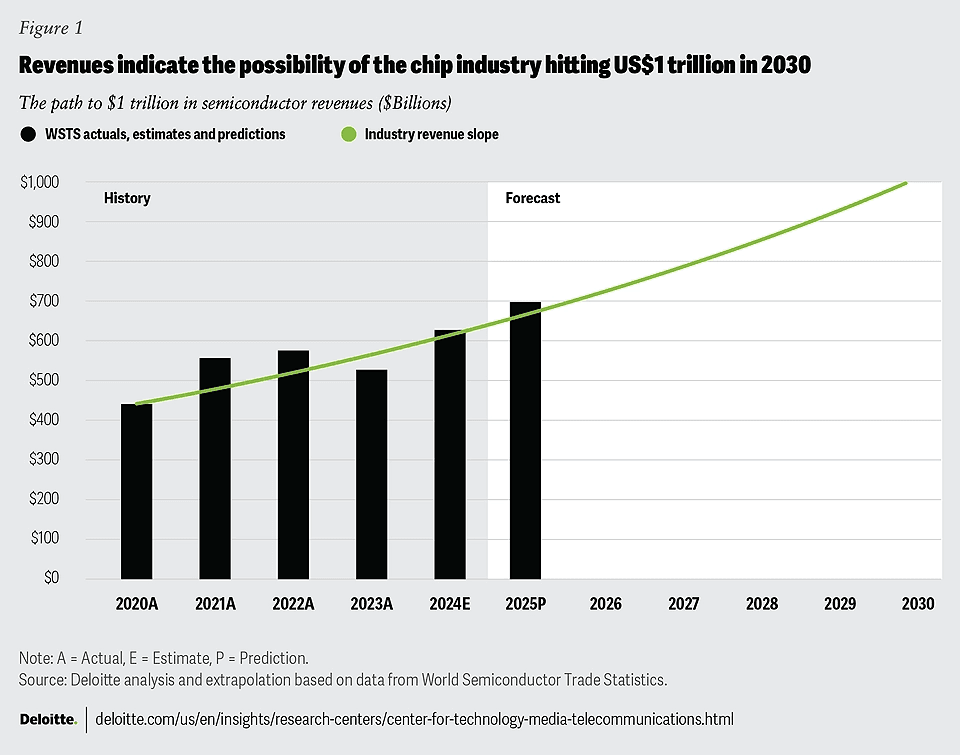

The semiconductor industry is experiencing exponential growth, particularly in AI, cloud computing, and high-performance computing (HPC). Hyperscaler demand for AMD’s EPYC CPUs remains strong, with public cloud EPYC instances increasing by 27% in 2024. Additionally, Forbes 2000 enterprises more than doubled their EPYC cloud consumption in Q4 2024, demonstrating AMD’s increasing enterprise adoption.

Source: deloitte.com

In the AI segment, AMD’s ROCm software enhancements have bolstered performance, making MI300X GPUs more competitive. More than 1 million models on Hugging Face now run on AMD, signaling growing developer adoption. The launch of MI325X, alongside upcoming MI350 and MI400 series GPUs, reinforces AMD’s long-term AI roadmap, which aims for double-digit billion-dollar revenue potential in the coming years.

Despite strong tailwinds, the outlook is tempered by recent estimate revisions. In the past three months, there were 20 downward EPS revisions compared to just 7 upward adjustments, alongside 12 downward revenue revisions. This suggests some uncertainty around near-term execution risks, possibly related to competitive pricing pressures or macroeconomic headwinds.

Source: Q4 Earnings Slides

*Disclaimer: The content of this article is for learning purposes only and does not represent the official position of SnowBallHare, nor can it be used as investment advice.