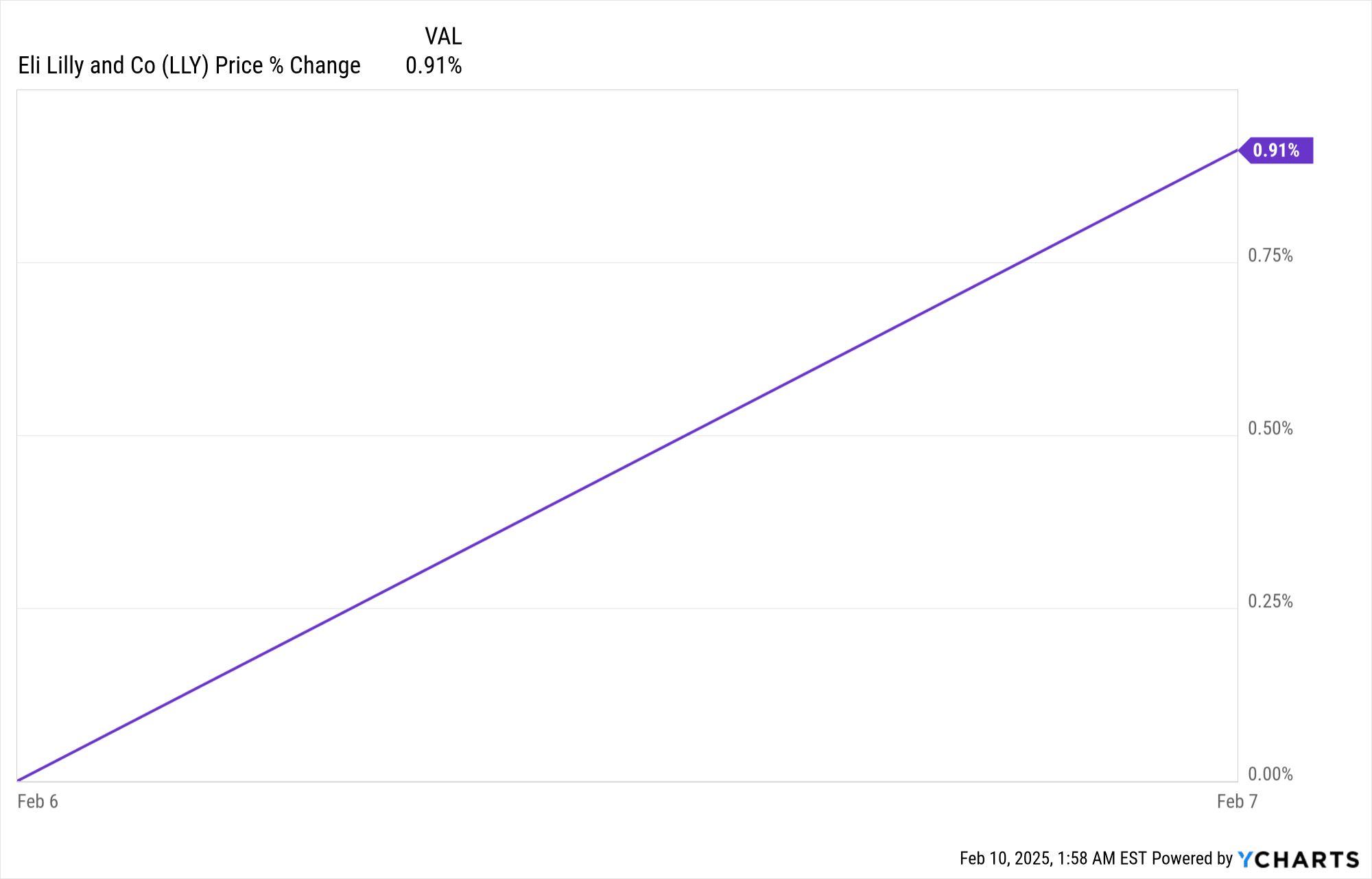

Eli Lilly’s (NYSE:LLY) stock price increased 1% post-earnings, reflecting a positive yet measured market reaction to its strong Q4 2024 results. Revenue of $13.53 billion exceeded expectations by $101.55 million, while normalized EPS of $5.32 surpassed forecasts by $0.25. Despite an operating income surge to $5.6 billion, a 26% rise in SG&A expenses due to product launches and an 18% increase in R&D costs tempered investor enthusiasm. The 5% decline in realized U.S. prices, despite a 45% volume surge, signaled pricing pressure. Analysts' mixed sentiment, with revised estimates and regulatory uncertainties, likely contributed to the stock's modest 1% gain.

Source: Ycharts.com

I. LLY Earnings Overview Q4 2024

Revenue vs. Expectations

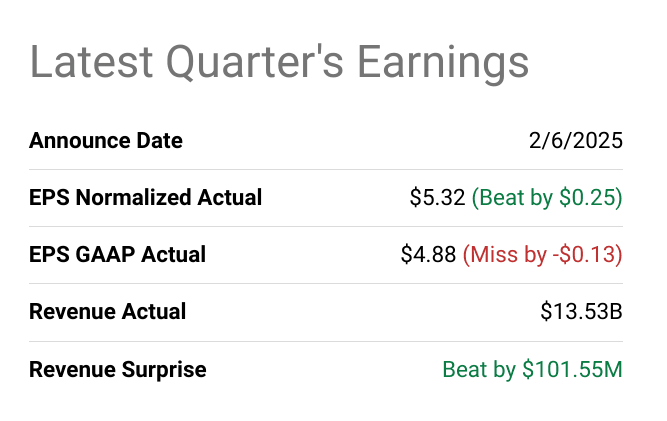

Eli Lilly and Company (LLY) delivered a strong Q4 2024 performance, with revenue of $13.53 billion, exceeding expectations by $101.55 million. Normalized EPS of $5.32 surpassed estimates by $0.25, while GAAP EPS of $4.88 missed by $0.13. Net income showed significant year-over-year (YoY) growth, reflecting robust market demand. Gross margin expanded to 83.2%, benefiting from a favorable product mix. Operating income more than doubled to $5.6 billion, driven by higher revenue and increased commercial investment. R&D expenses rose 18% due to extensive pipeline advancements, and SG&A expenses increased 26%, primarily attributed to promotional efforts for key product launches.

Source: seekingalpha.com

Eli Lilly Earnings Q4 2024 Revenue Drivers

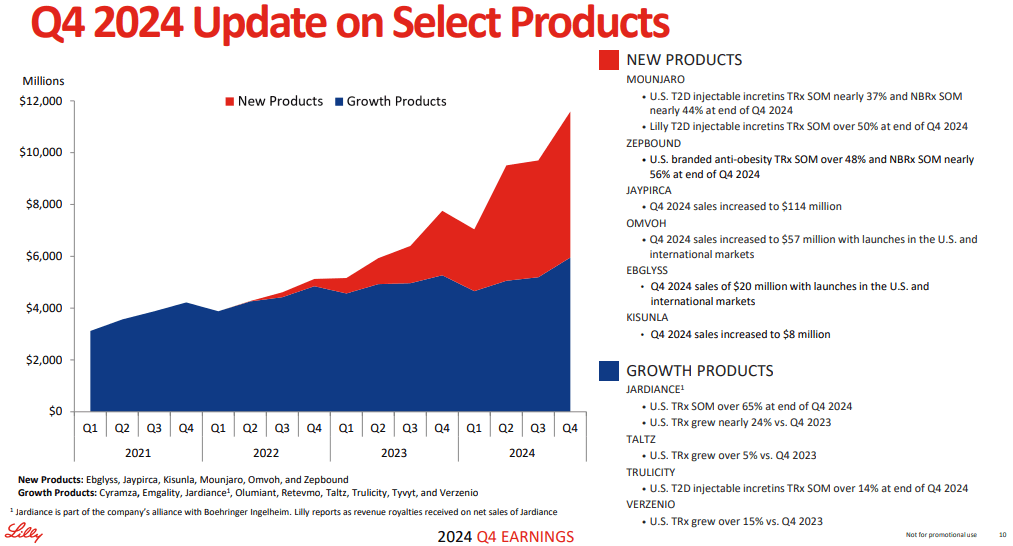

The company’s top-line growth was largely fueled by its incretin portfolio, particularly Mounjaro and Zepbound. Revenue from new products more than doubled to $5.6 billion, with Mounjaro generating $3.5 billion globally and U.S. Zepbound sales reaching $1.9 billion. U.S. revenue increased 40%, driven by a 45% volume growth despite a 5% decline in realized prices. European revenue surged 82% in constant currency, with 61% growth excluding a one-time payment. Japan and China posted 27% and 13% growth, respectively, largely driven by Mounjaro and Verzenio uptake. The company successfully launched Mounjaro in all major European markets and commenced a limited launch in China.

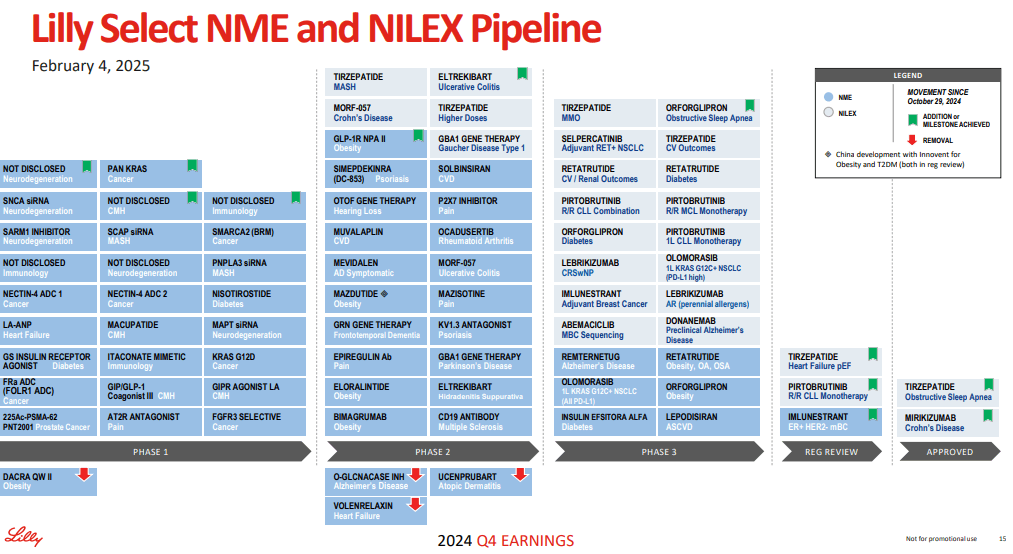

Regulatory milestones and R&D advancements further bolstered Eli Lilly’s market position. The company received approvals for Kisunla, Ebglyss, and a new Zepbound indication in obstructive sleep apnea. Submissions included tirzepatide for heart failure and imlunestrant for metastatic breast cancer. Eli Lilly initiated eight new Phase 3 programs in 2024 and expects further pipeline expansion in 2025. Investments in manufacturing, including expansions in Indiana, Wisconsin, and Ireland, have totaled $23 billion since 2020, strengthening supply capacity. Additionally, Eli Lilly returned $3 billion to shareholders via dividends and repurchases, with a new $15 billion share buyback program announced. The company projects 2025 revenue between $58 billion and $61 billion, with anticipated 32% YoY growth.

Source: Q4-24 Deck

II. Eli Lilly Product & Market Dynamics

Eli Lilly demonstrated strong product and market dynamics in Q4 2024, with significant revenue growth driven by key product launches, pipeline advancements, and strategic acquisitions. The company’s full-year revenue grew 32% year-over-year, exceeding its initial guidance by $4 billion. Quarterly revenue surged 45%, primarily fueled by Mounjaro and Zepbound, which contributed over $3.1 billion in new product revenue.

New Products & Innovations

Eli Lilly’s product pipeline advanced significantly, with regulatory approvals for Kisunla, Ebglyss, and a new indication for Zepbound in obstructive sleep apnea (OSA). The company also initiated Phase 3 trials for Lepodisiran, Remternetug, and Olomorasib, reinforcing its leadership in metabolic and neurodegenerative diseases. Key milestones included the submission of imlunestrant for metastatic breast cancer and tirzepatide for heart failure, both of which have the potential to drive significant revenue growth.

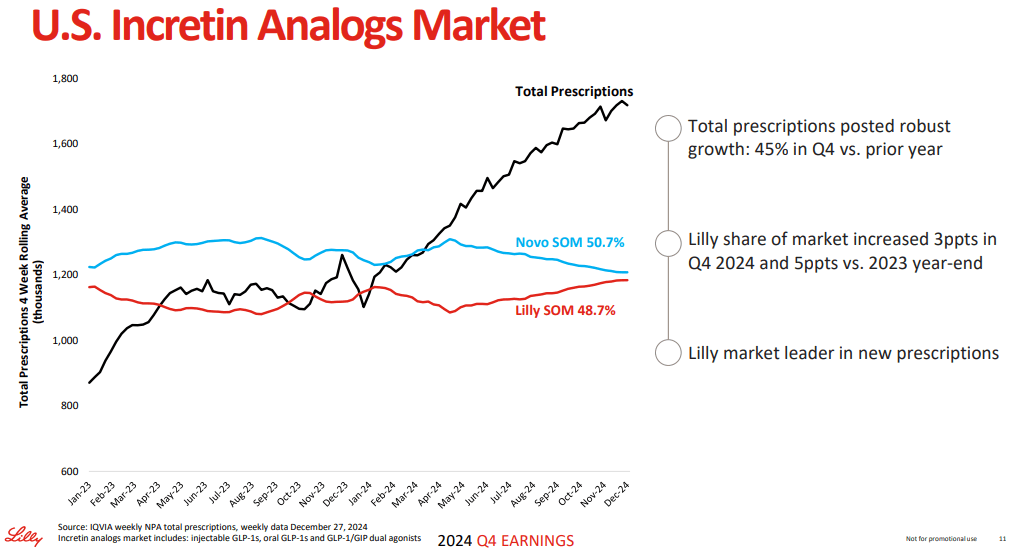

Mounjaro and Zepbound emerged as dominant players in their respective markets, with Mounjaro’s global sales reaching $3.5 billion in Q4, while U.S. Zepbound sales hit $1.9 billion. Notably, Zepbound became the U.S. market leader in the anti-obesity segment, as measured by new prescriptions. Meanwhile, Jaypirca achieved $114 million in worldwide revenue, and Omvoh, recently approved for Crohn’s disease, generated $57 million.

Source: Q4-24 Deck

The company expanded its genetic medicine capabilities through acquisitions and partnerships, including the purchase of Morphic Therapeutics and a collaboration with OpenAI to develop novel antimicrobials. Eli Lilly also launched the Seaport Innovation Center in Boston and the Lilly Gateway Lab in the UK to support research collaborations.

Competitive Landscape

Eli Lilly faces strong competition from Novo Nordisk, Merck, AbbVie, and Pfizer. Novo Nordisk’s Wegovy remains a key competitor in the weight loss market, though Zepbound’s superior 47% greater weight loss in the SURMOUNT-5 study positions it as a formidable rival. In diabetes, Mounjaro continues to erode market share from Trulicity and competing GLP-1 receptor agonists.

Pricing strategy remains a critical lever, with a 5% decrease in realized U.S. prices due to changes in rebates and discounts. However, volume growth of 45% in the U.S. mitigated pricing pressure, ensuring strong revenue expansion. Europe’s revenue surged 82% in constant currency, driven by Mounjaro’s successful launch across major markets. In China, the company saw a 13% revenue increase, though Mounjaro’s impact will be limited in early 2025 due to supply constraints.

With continued investment in manufacturing, including a $23 billion expansion since 2020, Eli Lilly aims to meet rising demand and strengthen its competitive edge. Looking ahead, the company anticipates 32% revenue growth in 2025, driven by increasing uptake of its incretin portfolio and the continued success of its oncology and neuroscience segments.

Source: Q4-24 Deck

III. LLY Stock Forecast

Eli Lilly Stock Forecast 2025 Technical analysis

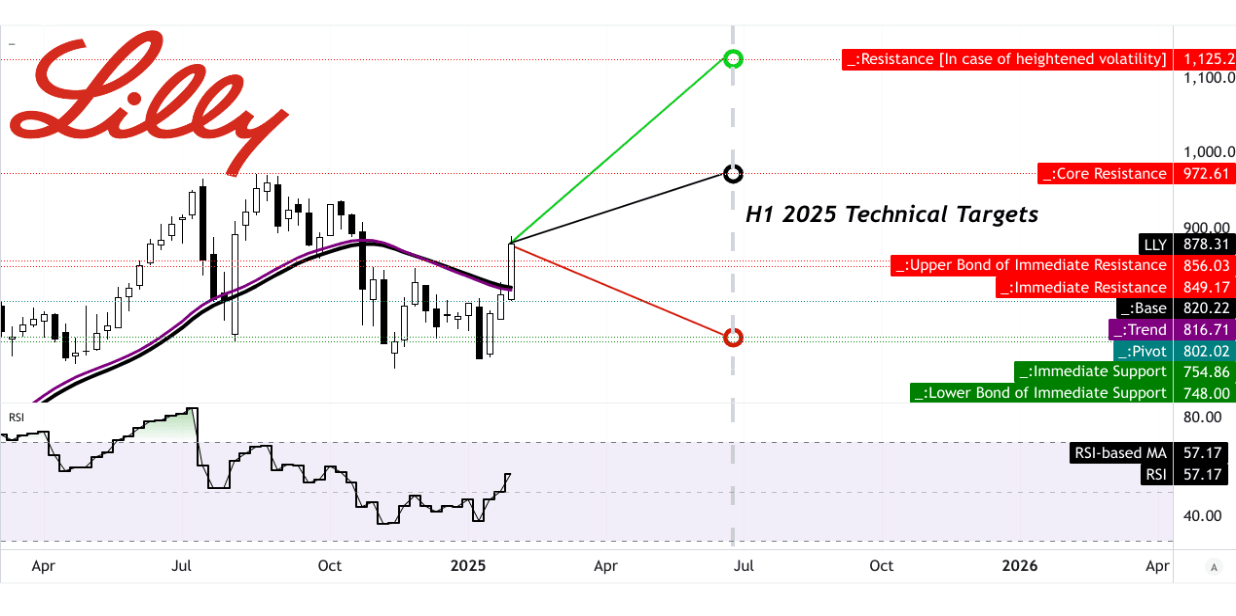

Eli Lilly's stock (LLY) currently trades at $878.31, with technical indicators suggesting continued upward momentum. The trendline, based on a modified exponential moving average, stands at $816.71, while the baseline is slightly higher at $820.22. The stock is currently trading above both levels, indicating bullish sentiment. Additionally, the pivot of the current horizontal price channel is set at $802.02, reinforcing a support level above which the stock has been consolidating. A key momentum indicator, the Relative Strength Index (RSI), stands at 57.17. This indicates that LLY is in a neutral-to-bullish phase, as it remains below the overbought threshold of 70 while showing an upward trend. There are no signs of bullish or bearish divergence, suggesting that the current price movement is consistent with market strength rather than speculative overextension.

Market analysts remain optimistic about LLY's trajectory. The average price target for the end of H1 2025 is set at $973.00, derived from the momentum of change-in-polarity over mid- to short-term periods and projected through Fibonacci retracement and extension levels. The optimistic price target is significantly higher at $1,125.20, suggesting that if LLY maintains its current bullish swing, it could experience substantial upside growth. Conversely, a pessimistic target of $755.00 reflects potential downside risk if market sentiment shifts or macroeconomic factors negatively impact the pharmaceutical sector.

Source: tradingview.com

LLY Stock Forecast: Market analysts' Expectations & Ratings

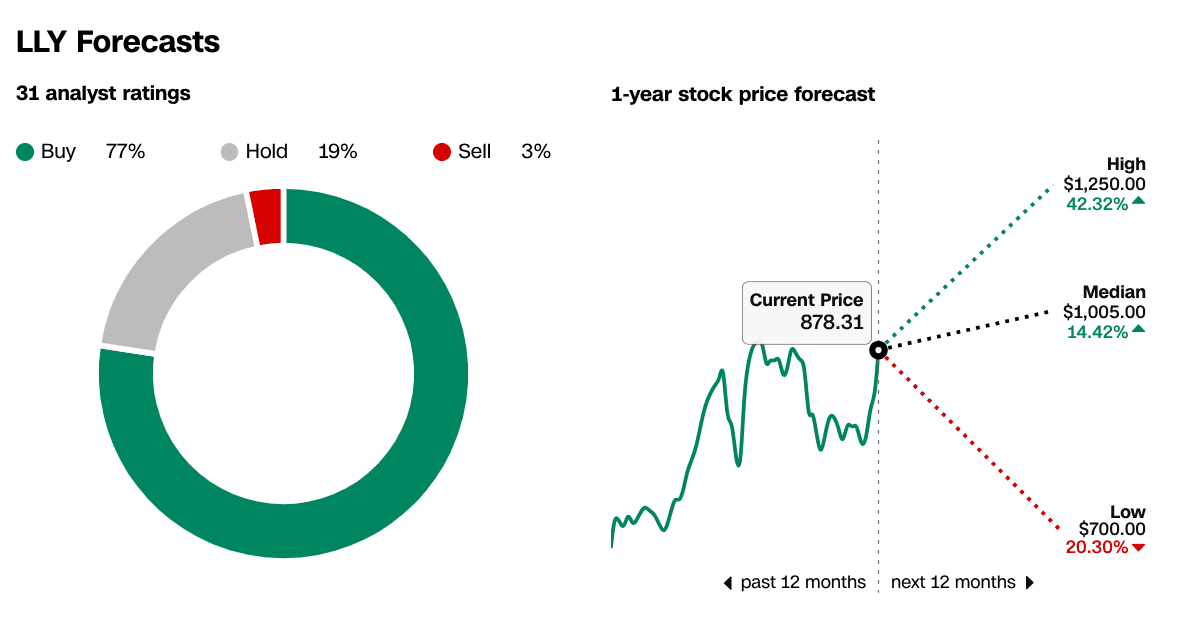

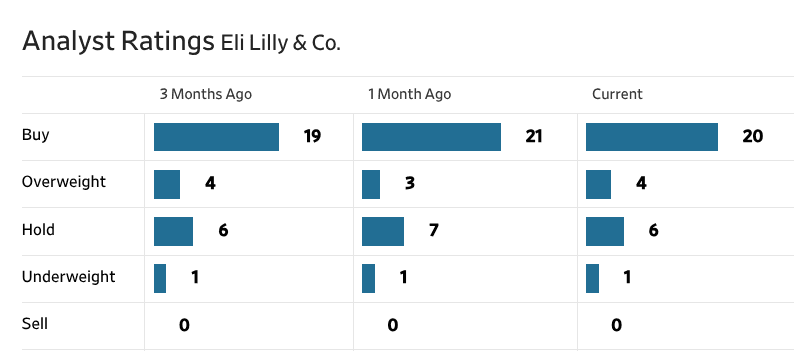

The next 12-month stock price forecast from 31 analysts ranges from a low of $700 (a decline of 20.30%) to a high of $1,250 (a potential 42.32% gain), with a median target of $1,005 (a 14.42% increase). Analyst ratings further reinforce a positive outlook, with 77% recommending a buy, 19% suggesting hold, and only 3% advising a sell. Over the past three months, buy ratings have remained strong, with minor fluctuations: three months ago, 19 analysts rated LLY as a buy, increasing to 21 a month ago before slightly retracting to 20 currently. The overweight rating has remained stable at 4, while hold ratings have fluctuated between 6 and 7. Importantly, no analysts have issued a sell recommendation, indicating broad confidence in LLY’s growth potential.

Source: CNN.com

Source: WSJ.com

IV. Eli Lilly Stock Forecst: Future Outlook

Management's Growth Forecasts And Strategic Initiatives

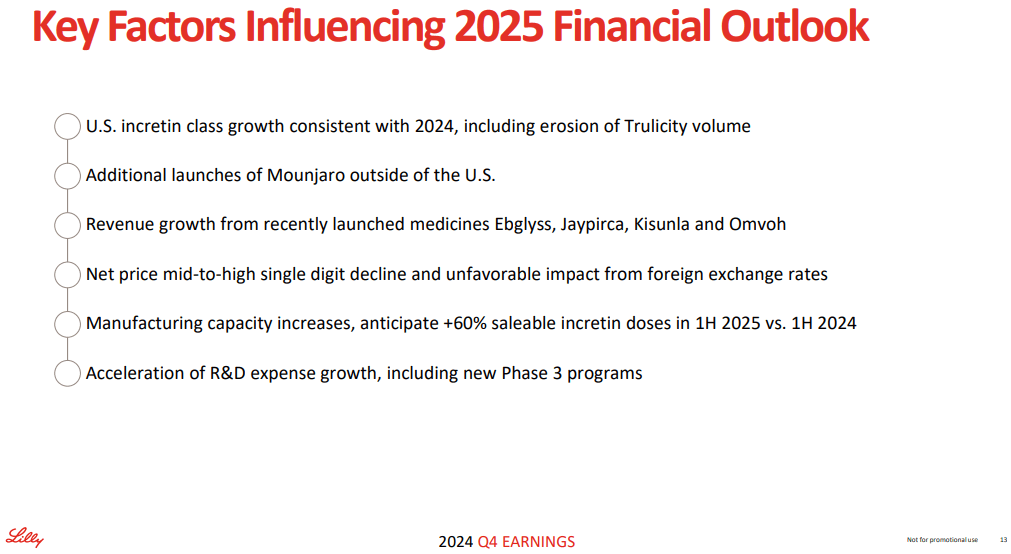

Eli Lilly’s stock outlook for 2025 appears promising, supported by strong growth forecasts and strategic initiatives. Management has provided optimistic revenue and earnings guidance, projecting Q1 2025 earnings per share (EPS) of $4.72, an 82.90% year-over-year (YoY) increase, and revenue of $12.75 billion, reflecting a 45.43% YoY growth. Despite these strong projections, analysts have revised EPS and revenue estimates downward twice in the past three months, suggesting some caution in expectations.

Key drivers of growth include continued expansion in the incretin drug market, where Eli Lilly’s Mounjaro and Zepbound have demonstrated significant sales momentum. Mounjaro’s international rollout is expected to contribute meaningfully to revenue growth in the latter half of 2025, complementing U.S. sales. However, the anticipated erosion of Trulicity’s volume remains a headwind. The company is also set to benefit from recently launched medicines, including Ebglyss, Jaypirca, Kisunla, and Omvoh, which are expected to drive additional revenue streams. Manufacturing capacity expansion is another pivotal factor, with a projected 60% increase in saleable incretin doses in the first half of 2025 compared to the same period in 2024, ensuring supply meets rising demand.

Source: Q4-24 Deck

Market Trends

Strategic investments in research and development (R&D) further bolster long-term growth prospects. The company is accelerating its R&D spending, including new Phase 3 programs, signaling confidence in future product innovations. Recent acquisitions, such as Morphic Therapeutics and the collaboration with OpenAI to develop novel antimicrobials, highlight Eli Lilly’s focus on pipeline expansion. Additionally, regulatory approvals for new indications, such as Zepbound for obstructive sleep apnea and Omvoh for Crohn’s disease, enhance its market position.

However, macroeconomic and regulatory factors pose potential risks. Drug pricing pressures, mid-to-high single-digit net price declines, and unfavorable foreign exchange rates could negatively impact profit margins. The company has also forecasted a tax rate increase to 16%, which may slightly offset earnings growth. Despite these challenges, Eli Lilly’s focus on expanding its portfolio, increasing manufacturing capabilities, and maintaining strong revenue growth positions it well for sustained stock performance in 2025.

Source: iqvia.com

*Disclaimer: The content of this article is for learning purposes only and does not represent the official position of SnowBallHare, nor can it be used as investment advice.