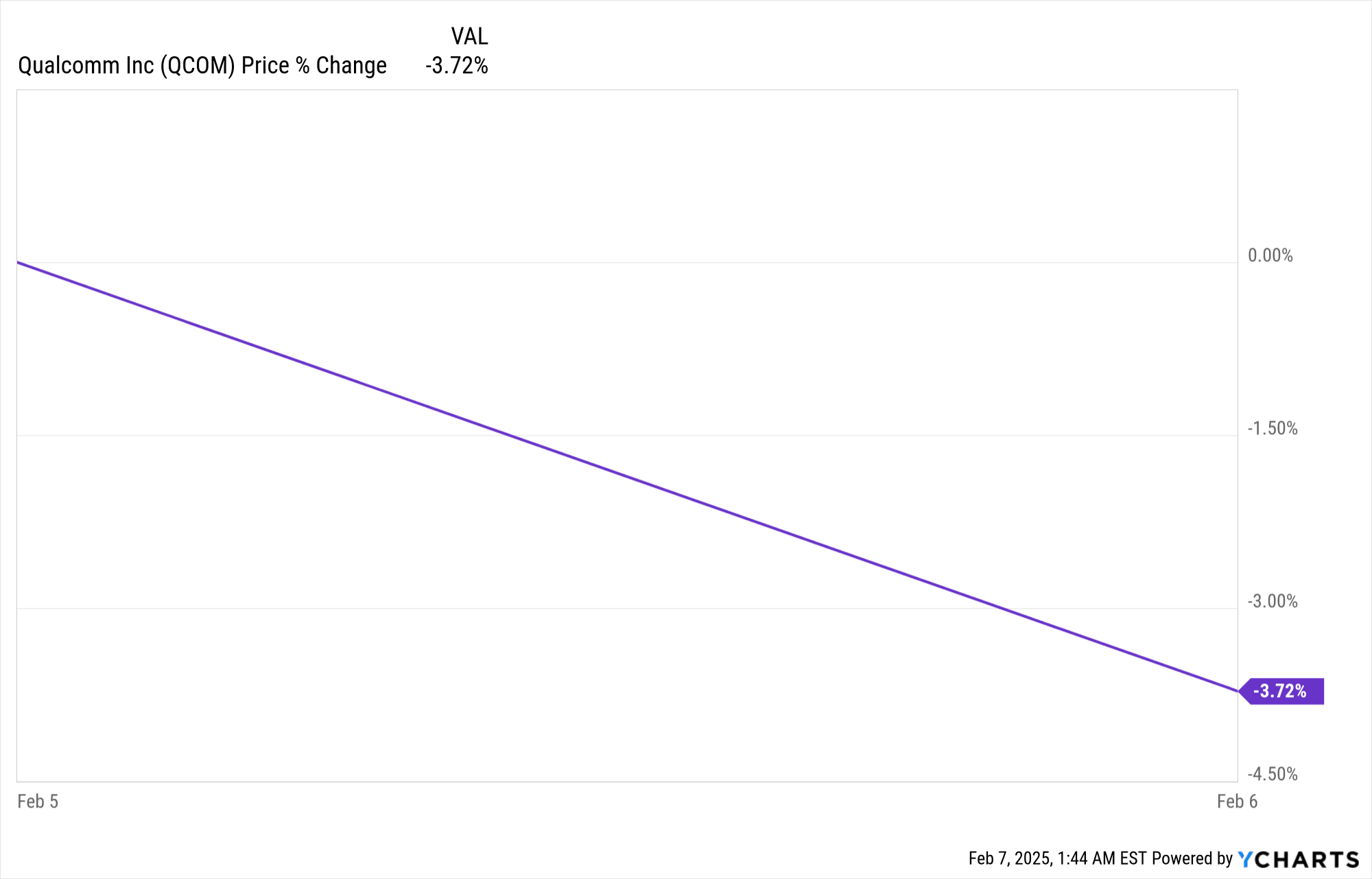

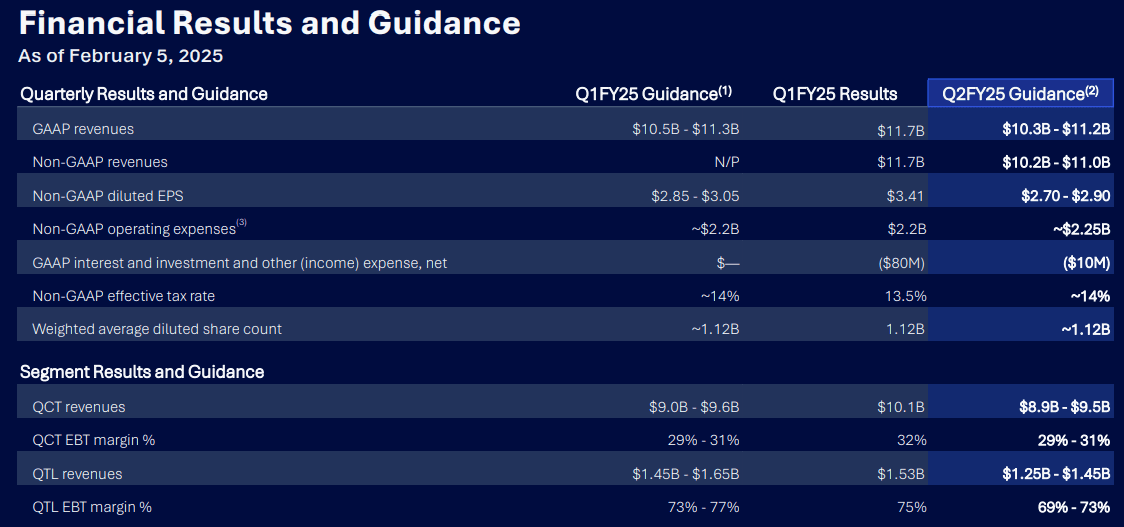

Qualcomm stock (QCOM) declined 3.7% post-earnings despite record Q1-25 revenue of $11.67B (+6.7% YoY). Non-GAAP EPS exceeded forecasts by $0.42, reaching $3.41, but guidance projected slower Q2 growth ($10.2B-$11B revenue, $2.70-$2.90 EPS). Concerns over smartphone dependency and competitive risks offset gains in AI, automotive (+61% YoY), and IoT (+36% YoY), pressuring investor sentiment.

Source: Ycharts.com

I. QCOM Earnings Overview Q1 2025

Earnings vs. Expectations

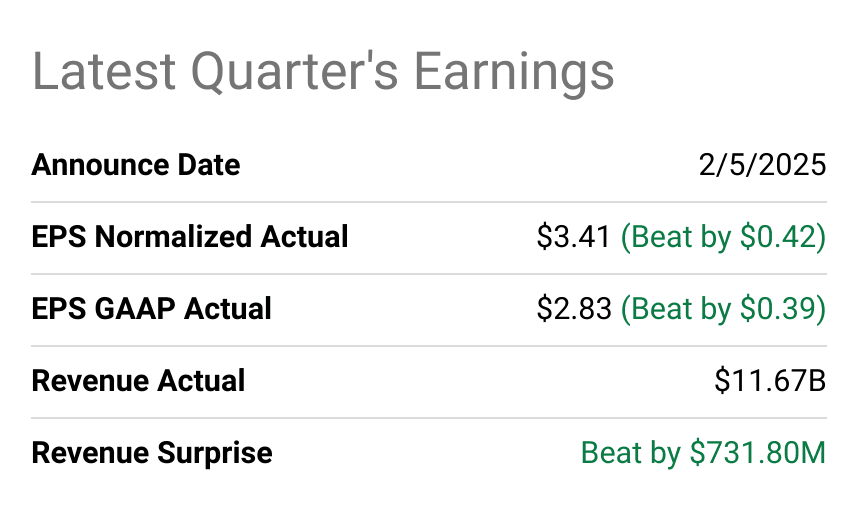

Qualcomm (QCOM) reported record Q1-25 earnings, surpassing expectations across key financial metrics. The company generated $11.67B in revenue, exceeding forecasts by $731.8M. Non-GAAP earnings per share (EPS) reached $3.41, beating estimates by $0.42, while GAAP EPS came in at $2.83, surpassing expectations by $0.39. Net income showed strong YoY growth, supported by record-breaking revenue in its chipset (QCT) division and robust licensing (QTL) performance. Gross margin trends remained stable, while operating and net margins expanded due to improved efficiency and higher-margin products, particularly in automotive and IoT.

Source: seekingalpha.com

Qualcomm Earnings Q1 2025 Revenue Drivers and Market Performance

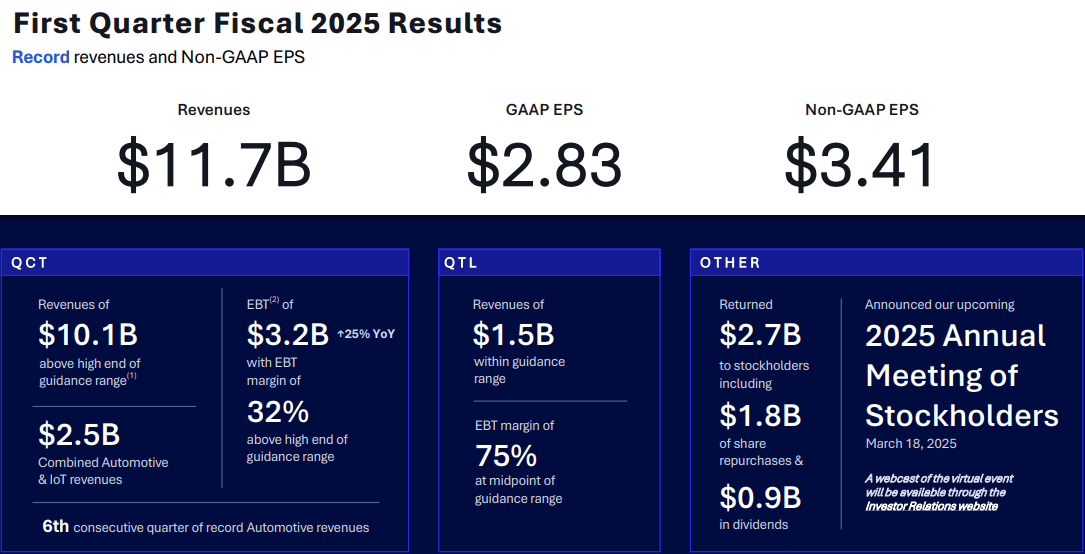

The QCT segment recorded an unprecedented $10.1B in revenue, marking its first-ever quarter exceeding $10B. Within QCT, handsets generated $7.6B (+13% YoY), driven by strong Snapdragon 8 Elite adoption in Samsung Galaxy S25 and Chinese flagship smartphones. Automotive revenue soared 61% YoY to $961M, marking the sixth consecutive record-breaking quarter. IoT revenue increased by 36% YoY to $1.5B, benefiting from on-device AI advancements. The QTL segment contributed $1.5B, with an Earnings Before Tax (EBT) margin of 75%, aligning with expectations. Licensing revenue stability, bolstered by new long-term agreements with major Chinese OEMs, secures revenue consistency for FY25.

Source: Q1-FY25 Deck

AI and Strategic Growth Initiatives

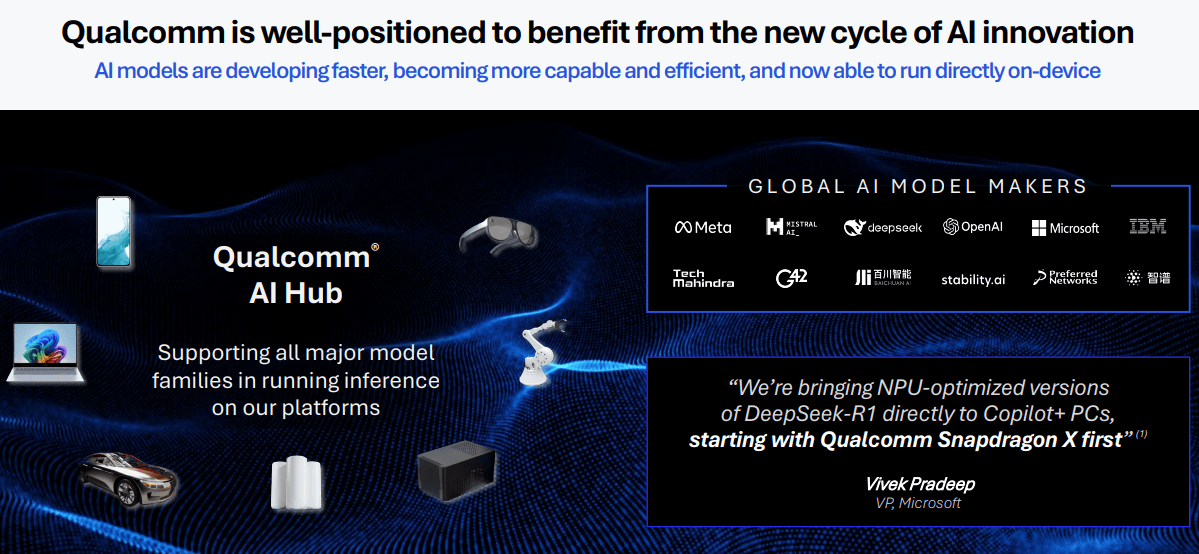

Qualcomm emphasized AI-driven opportunities, particularly edge AI inference. The Snapdragon 8 Elite’s integration into flagship devices, featuring AI-enhanced capabilities, highlights its leadership in premium-tier smartphones. The rapid deployment of DeepSeek-R1 on Snapdragon-powered devices underscores Qualcomm’s agility in AI adoption. PC expansion gained momentum with over 80 Snapdragon X designs in progress, targeting over 100 by 2026. The introduction of the Snapdragon X for the $600 PC market expands Qualcomm’s addressable opportunity. Automotive traction continued with expanded partnerships, including Hyundai Mobis, Panasonic Automotive, and Garmin. The Snapdragon Digital Chassis Workbench launch strengthens its software-defined vehicle positioning.

II. Qualcomm Product & Market Dynamics

New Products & Innovations

Qualcomm’s Q1-25 delivered record revenues based on aggressive expansion into the AI-driven edge computing, automotive, and IoT markets. In new products and innovations, Qualcomm’s Snapdragon 8 Elite for Galaxy has positioned itself as a premier mobile platform. The global deployment of this chipset in Samsung’s Galaxy S25 series underscores its competitive strength in the premium smartphone segment. Qualcomm's AI capabilities are advancing rapidly, demonstrated by the integration of DeepSeek-R1 AI models on Snapdragon-powered devices within days of release. The company's edge AI strategy reflects an industry-wide shift toward on-device inference, enhancing efficiency and accessibility.

Source: Q1-FY25 Deck

Qualcomm’s push into the PC market through the Snapdragon X series is also gaining momentum. With over 80 designs in production or development and expectations of surpassing 100 designs by 2026, the company is expanding its footprint in AI-driven computing. The introduction of the Snapdragon X, targeting the $600 PC segment, further broadens Qualcomm’s addressable market. Consumer reception for Snapdragon X has exceeded expectations, capturing over 10% market share of Windows laptops priced above $800 in the U.S. retail market as of December 2024, according to Circana.

The automotive market remains a significant growth driver, with Qualcomm’s QCT automotive revenues soaring 61% YoY to $961M. Strategic collaborations with Hyundai Mobis, Leapmotor, and Mahindra highlight the growing adoption of Snapdragon digital chassis solutions. Additionally, partnerships with Panasonic, Garmin, and Desay SV signal Qualcomm’s expansion into AI-powered in-cabin and driver assistance systems. The launch of the cloud-based Snapdragon Digital Chassis Workbench further strengthens its position in the software-defined vehicle ecosystem.

IoT and industrial applications also present a lucrative opportunity. Qualcomm reported a 36% YoY growth in IoT revenues, driven by AI-enabled consumer networking and industrial applications. The launch of AI on-premise appliances at CES 2025 and partnerships with Honeywell and IBM reinforce its leadership in enterprise AI solutions. Qualcomm Aware, its cloud-based asset visibility platform, is gaining traction across industries such as energy, manufacturing, and logistics.

Competitive Landscape

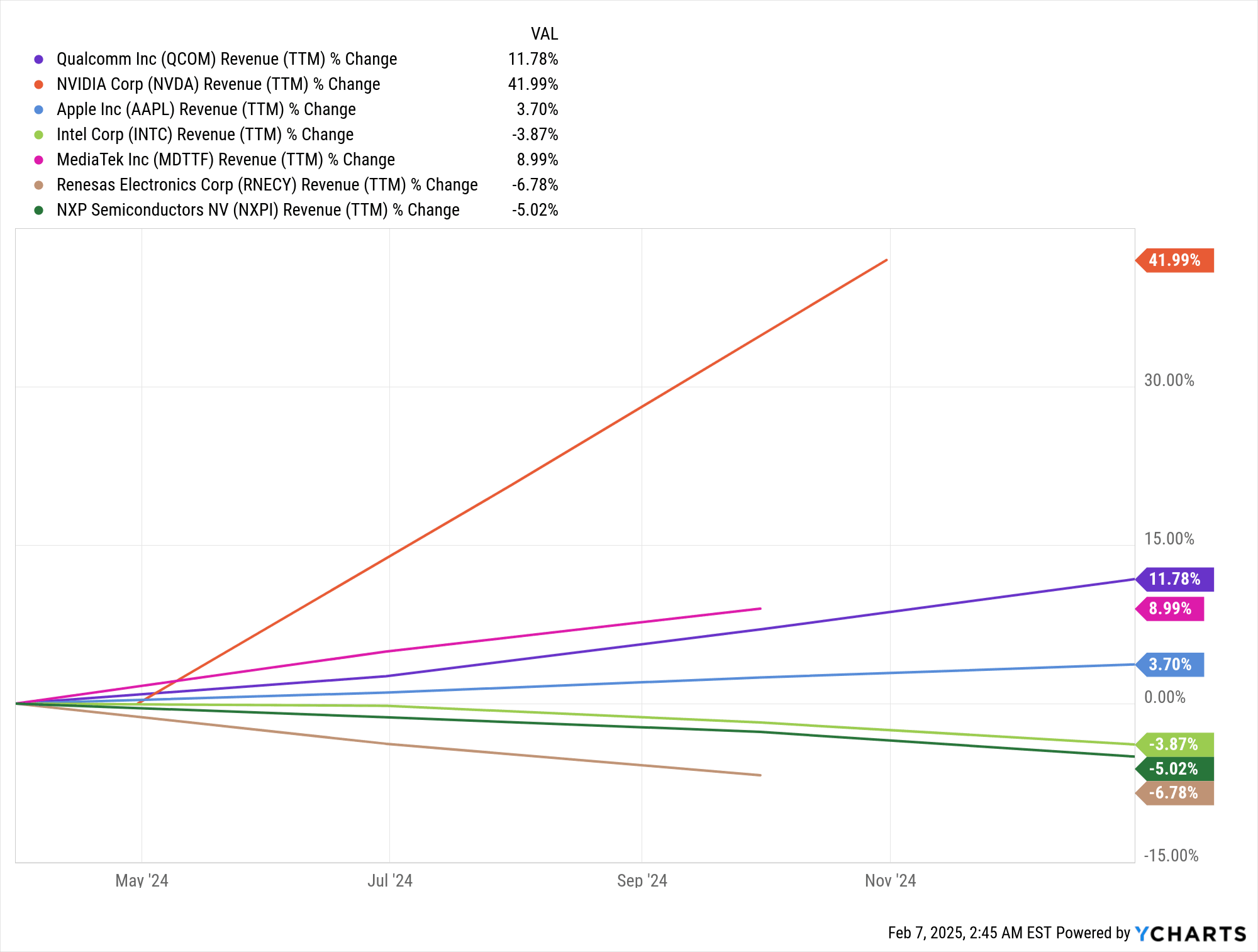

The competitive landscape remains intense. Qualcomm faces stiff competition from MediaTek in mid-tier smartphones, while Apple’s in-house silicon threatens its premium market share. Intel and Nvidia continue to dominate in high-performance computing, but Qualcomm’s AI-focused strategy in edge computing provides a differentiated value proposition. In the automotive sector, Qualcomm is battling Nvidia and traditional chipmakers like Renesas and NXP. Pricing strategies remain aggressive, with Qualcomm leveraging strategic partnerships and advanced AI capabilities to maintain leadership. As the AI-driven computing era evolves, Qualcomm’s diversified product portfolio provides a stable top-line against its competitors.

Source: Ychart.com

III. QCOM Stock Forecast 2025

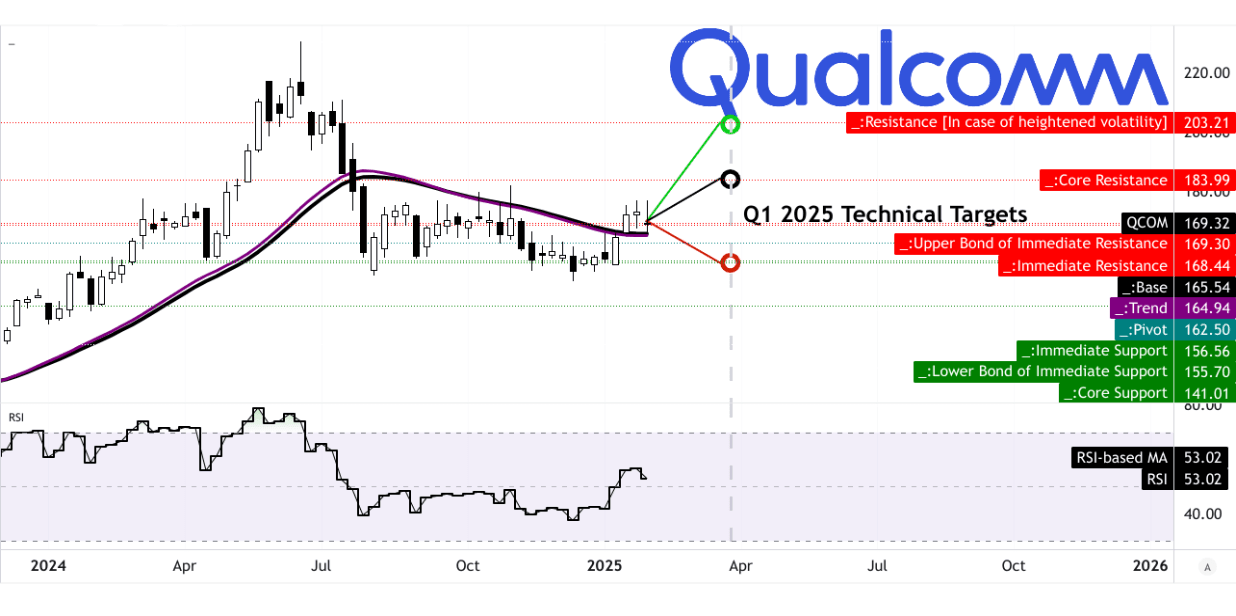

Qualcomm Stock Forecast Technical Analysis

As of now, QCOM stock trades at $169.32, with a trendline at $164.94 and a baseline at $165.54, both calculated using a modified exponential moving average. The stock is currently positioned within a horizontal price channel, with a pivot level at $162.50. A key technical indicator, the Relative Strength Index (RSI), stands at 53.02, indicating neutral momentum without any significant bullish or bearish divergence. However, the RSI line is trending upward, suggesting a gradual increase in buying pressure.

From a price projection standpoint, analysts expect QCOM’s average price target to reach $184 by the end of Q1-25 . This forecast is based on momentum shifts and Fibonacci retracement/extension levels. In a more optimistic scenario, where the current upward price momentum continues, QCOM stock price could reach as high as $203. Conversely, if downward pressure emerges, the stock could decline to a pessimistic target of $157. These projections rely on technical indicators assessing short- to mid-term price swings.

Source: tradingview.com

QCOM Stock Forecast: Market Analysts' Expectations & Ratings

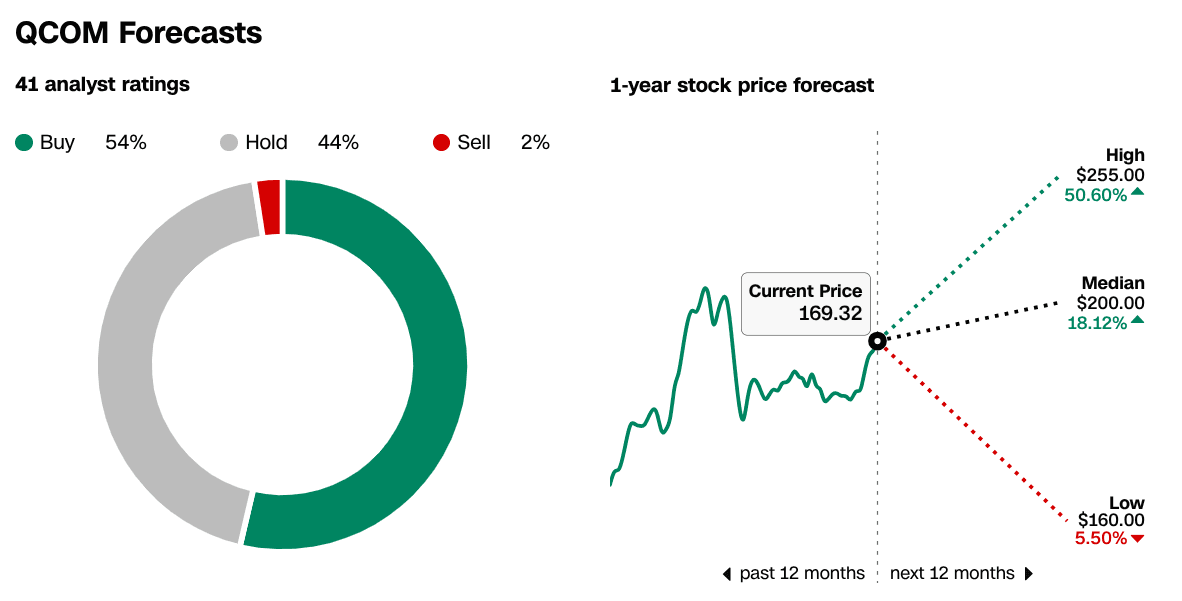

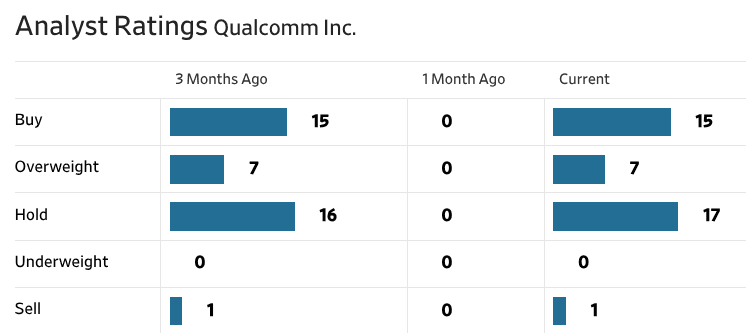

Market analysts provide a range of expectations for Qualcomm stock over the next 12 months. Among 41 analysts, 54% rate QCOM as a “Buy,” while 44% recommend “Hold,” and only 2% suggest “Sell.” The stock’s 12-month price target ranges from a high of $255, representing a 50.6% potential upside, to a low of $160, a modest 5.5% decline from the current Qualcomm stock price. The median target sits at $200, implying an 18.12% gain. Notably, sentiment among analysts has remained stable over the past three months, with 15 “Buy” ratings, seven “Overweight” ratings, 17 “Hold” ratings, and only one “Sell” rating.

Source: CNN.com

Source: WSJ.com

IV. Qualcomm Stock Forecast: Future Outlook

Management's Growth Forecasts And Strategic Initiatives

Qualcomm’s future outlook is driven by management’s strong growth forecasts, strategic initiatives, and evolving market trends. The company delivered record-breaking Q1-25 earnings and revenues. The chipset division (QCT) contributed significantly with substantial growth in handsets ($7.6B), automotive (61% YoY growth), and IoT (36% YoY growth). Management remains committed to achieving $22B in non-handset revenues by 2029, with a focus on AI, edge computing, and automotive applications.

For Q2 2025, Qualcomm has provided revenue guidance between $10.3B and $11.2B, with non-GAAP EPS expected between $2.70 and $2.90. This represents a 12.39% YoY revenue increase and a 14.47% rise in EPS. Market analysts have responded positively, with 17 upward revisions for EPS and 14 for revenue over the last three months, indicating strong confidence in Qualcomm’s growth trajectory. This optimism is fueled by the continued success of the Snapdragon 8 Elite for Galaxy, which powers the Samsung Galaxy S25 series, as well as increasing design wins among Chinese smartphone OEMs and PC manufacturers.

Source: Q1-FY25 Deck

Market Trends

Beyond mobile, Qualcomm is making significant strides in AI and computing. The Snapdragon X series is gaining traction in the PC market, with over 80 designs in development and more than 100 expected by 2026. The introduction of the Snapdragon X platform for mid-range PCs further expands the company’s addressable market. Additionally, Qualcomm has entered the AI-driven smart glasses market with the Snapdragon-based Ray-Ban Meta glasses, which are exceeding expectations. AI-powered applications are also expanding in the Windows ecosystem, with over 50 AI apps optimized for Snapdragon.

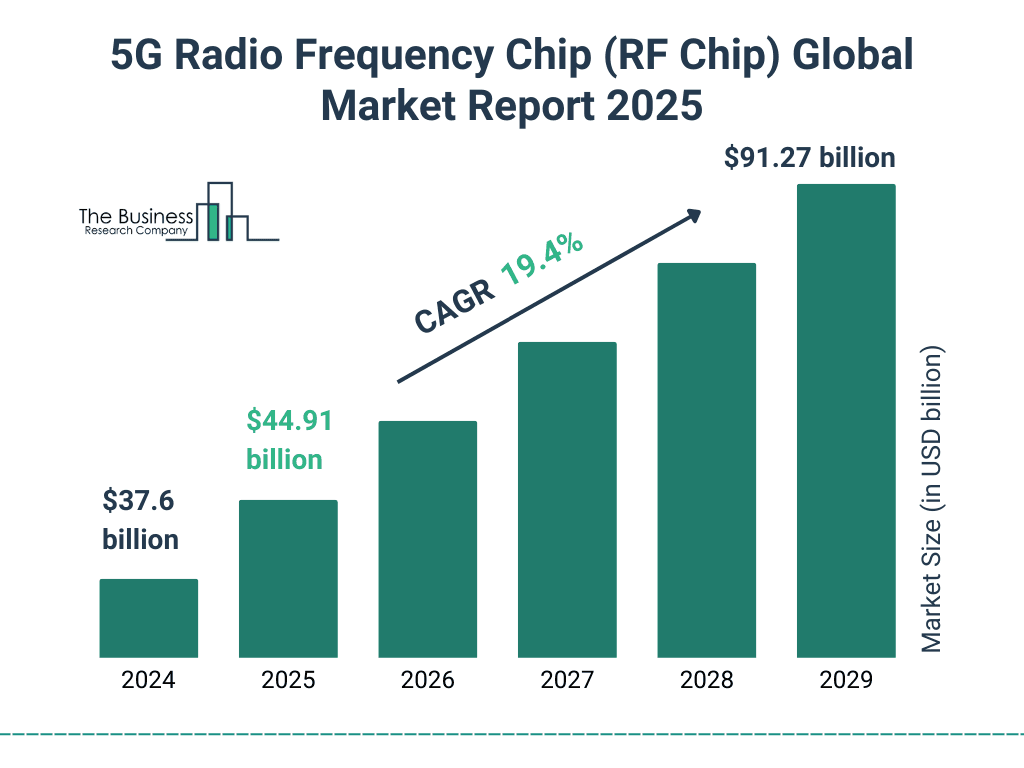

In the automotive sector, Qualcomm is strengthening its position as a leader in software-defined vehicles, partnering with major automakers such as Hyundai Mobis, Leapmotor, and Mahindra. The Snapdragon Digital Chassis platform is becoming a key component for AI-powered in-cabin experiences and driver assistance systems. Meanwhile, 5G and Wi-Fi 7 adoption continue to drive growth in edge networking, with operators in North America and India deploying Qualcomm’s fixed wireless access solutions.

Source: thebusinessresearchcompany.com

*Disclaimer: The content of this article is for learning purposes only and does not represent the official position of SnowBallHare, nor can it be used as investment advice.